THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES. FOR MORE INFORMATION.

Learning how to budget is a critical part of personal finance.

If you have no idea where your money is going, you are going to have a hard time reaching your financial goals.

But as important as a budget is, most people avoid the practice at all costs.

The biggest reason is because they don’t want to be told how to spend their money.

They want the freedom to buy what they like and not feel restricted or guilty.

But you can spend money how you want, not feel guilty, and reach your money goals with a budget.

And this post is going to show you how.

I’ll walk you through how to start budgeting so you can keep track of your spending.

And for some of you, seeing your spending habits is going to amaze you.

Don’t be surprised if you are blown away at how much money you spend on certain things.

So let’s get started with building a simple budget for you to begin to take control of your financial life.

How To Start Budgeting | The Ultimate Guide

Before we get into the steps to building a budget, we first need to cover some important issues you will face.

The first thing to know is have patience.

No matter what information you have, you won’t get your budget entirely right the first time.

Or likely even the second.

You have to be willing to make adjustments for probably two to three months before you get a handle on things.

And even then, you’ll be making tweaks as the months pass and life happens.

Take me for example.

In my life, I’ve used 4 different types of budgets until I found the one that works for me.

- Read now: Discover 17 budgeting methods to try

The key is to not get discouraged, but to learn from the budget.

What worked for you and what didn’t?

By asking yourself these questions, you will get closer to finding the right budget for you.

The second thing to know is have perseverance.

Don’t give up because your first budget is wildly off.

Your first budget is the one where we finally learn how much we really spend and what we really spend our money on.

Many of us aren’t aware that our Starbucks habit really is that bad.

Don’t beat yourself up about how much you spend or how you spend.

The goal here is to make a spending plan going forward.

The third thing to know is there are different ways to budget.

Some people prefer using pen and paper, writing everything down.

Others prefer Microsoft Excel or other spreadsheet programs to help make the process of budgeting easier.

Still others prefer using budgeting apps that automate the entire process.

You have to figure out what system works best for you and your goals.

The final thing to know is it’s all about details.

Your budget will be as detailed as you like.

Some people prefer to categorize every single expense and keep tabs on things over time.

Other people like to keep it simpler, and just track discretionary spending.

You have to figure out what works best for you and not think that your way is wrong if it works for you.

Now it is time to sit down and set up a budget.

I’ll detail how to create a basic budget using Microsoft Excel.

If you prefer to use pen and paper, it will be virtually identical to what I walk you through below.

Just remember to keep these points in mind as you travel down the budgeting road.

Step #1: Determine Your Income

The first part of any budget is to determine how much money you are bringing into the budget.

To keep things simple, just take your monthly income and total it up.

For this post, I am using your net income to budget with.

Some people prefer to use their gross income and keep track of the income taxes they pay, as well as health insurance premiums, and other pre-tax deductions.

If you want to track these things, you can.

I am not just so it is easier to follow along.

To get your number, just look at the net pay amount from your regular paycheck and multiply this by how often you are paid in a given month.

If you are self-employed, then take out all of your withholdings, any 401(k) contributions, self-employment tax payments made, etc., to get to your net pay number.

Your net pay number is the amount of money you have available for saving and spending in your monthly budget.

If you work a sales job or earn commissions and you have irregular income, use a conservative estimate for your income.

If you earn a base salary, you might want to just budget this amount and then have a separate budget for your commission.

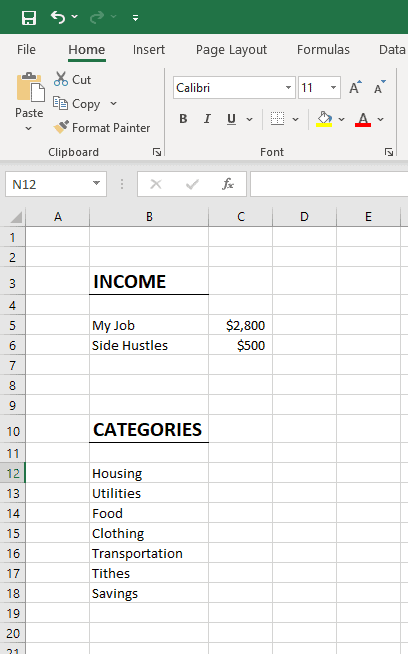

Below is what your budget should look like.

Step #2: Create Categories

Now that you have your income number listed, it is time to take a look at expenses.

Below your income, start writing general categories for expenses.

A desired order would be in the order of importance.

In other words, if you have very limited money and you just had to use it for certain things, what would those most important categories be?

Here’s a hint, put down these 7 categories first:

- Housing: Rent or mortgage, property taxes, maintenance, any HOA dues, etc.

- Utilities: Cable, electric, water, trash, cell phone bill

- Food: Separated into groceries and restaurants

- Clothing: Basic, only what you need

- Transportation: Car loan, bus/transit fares, tires, repairs, gas, oil changes, registration fees, etc.

- Tithes/Giving: Charity is always important

- Savings: Put something away for emergencies or to help pay off debt

This is just a small sample of the categories you can use.

Most people also include an entertainment category, personal care category, and a miscellaneous category.

You can even break out some of the categories into more categories too.

If you need a new category for something that does not fit one of the above categories, make one like credit card debt, student loan debt, personal care and so on.

For example, maybe you want a groceries category and a dining out category.

- Read now: Here is how to spend less on groceries

When you are finished with this step, your budget should look something like the below image.

Note that I added in a household category since I have expenses that didn’t fit under the 7 main categories.

For me, household expenses are anything I buy for around the house, like cleaning supplies and personal care items.

Again, you set up categories that make the most sense for you.

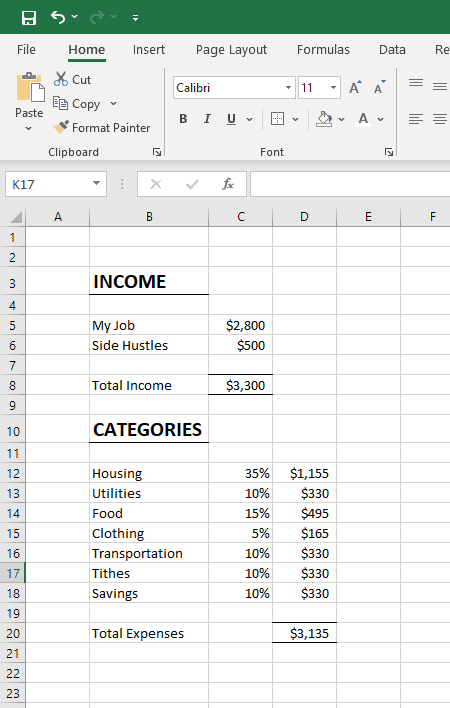

Step #3: Assign Spending Amounts

Now that you have your categories, it is time to assign spending amount to each one.

To the right of your budget categories, you will place the spending amounts.

This is where you need to have an open mind.

The numbers you put down here are going to be way off for most of you, since you have no idea how you spend your money.

Just take your best guess here and be open to the fact they next month you will have to make adjustments.

If you want to get a little closer to what you actually spend, you can review previous months credit card statements and bank statements.

Take all of the spending, categorize it, and total it up to get an idea of how you spend money.

Another option is to use a general guideline for how much to spend in each category.

Below is a rough guide you work with.

- Housing: 25-35%

- Utilities: 7-10%

- Food: 10-15%

- Clothing: About 5%

- Transportation: 5-10%

- Tithes/Giving: About 10% of your take-home pay

- Savings: 10% to start, more as you pay off debt

For example, if your take home pay is $3,000, by this guideline you would budget up to $300 to your church or favorite non-profit.

You would put $300 in savings and spend up to $1,050 for housing.

From there you can spend up to $300 for utilities, $450 for food, $300 for transportation and $150 for clothing.

Again, these are guidelines.

Bills have to be paid, so you should fully fund those expenses first and then adjust other categories accordingly.

If you have to skip tithing for a month, fine.

But don’t leave the savings column blank too.

You have to pay yourself in some way, and savings is important especially if you don’t have much savings to speak of anyway.

- Read now: Discover the simplest way to become rich

Don’t leave savings blank. Ever.

Even if you can only save 1% because money is tight, save that 1%.

Here is a sample of what your budget should look like at this point.

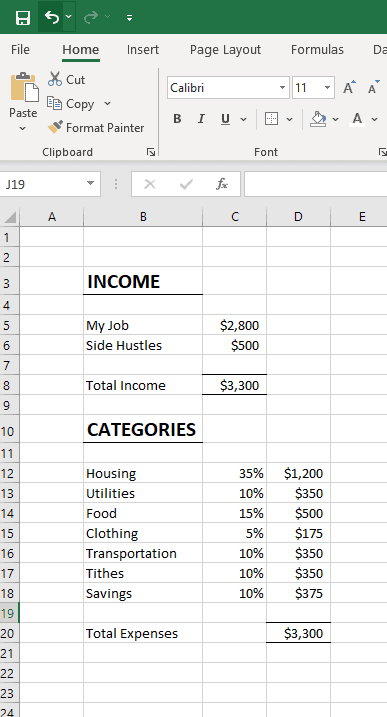

Step #4: Zero It Out

Having your money allocated into each category is great, but now you have to make the final adjustments.

This is because the total of your outgoing money has to equal your take-home pay so when you subtract expenses from income the resulting number is zero.

This is called zero-based budgeting or zero sum budgeting, and the goal is to make sure that every dollar that is coming in is labeled as it goes out.

Every. Single. Dollar.

If you actually have a positive number when you do the math, that means you have room to add money into some categories.

Ideally this money should go towards making extra debt payments or adding it into savings.

If you have a negative number left, that means you allocated too much money in the categories, so you will need to make some cuts.

Review your list of categories and see where you can cut back.

I recommend you pick categories that have the most discretionary spending or wants, as you can lower these expenses and still enjoy life.

Finally, you might find some categories don’t need a dollar amount every month.

For example, if you don’t think you will need clothes for this month, you can either leave it blank or put in any amount, like $20 as a placeholder.

This helps when it comes to unexpected expenses, which I get into later.

It is also a way to help you save for non-monthly bills, like car insurance.

You can divide your annual car insurance premium by 12 months and put aside that amount every month to pay the bill when it comes due every six months.

Just make sure to move that money into a separate savings account so when the bill does come, you have the cash to pay it.

Step #5: Start Tracking Your Spending

Now that you have your budget set up, it is time to follow it by tracking your spending for a month.

Keep track of all your expenses during the month, keeping every receipt and entering every expense into the appropriate category.

I’ve found that what works best for me is to collect receipts on a corner of my desk for a week.

Then on the weekend, I sit down for 15 minutes and update our budget.

I’ve found doing this really helps me to make budgeting a habit.

When I was waiting until the end of the month, it was overwhelming having to go through a mountain of receipts.

Plus, when I waited so long to update my budget, it really wasn’t helping me until it was too late.

What I mean by this is, at the end of the month I would see I blew my eating out budget on fast food halfway through the month.

Since I didn’t update my budget, I kept spending money eating out, making things worse.

Had I updated my budget more often, I could have cut back spending in the area and saved myself some money.

So now I update my budget weekly.

Another thing is that in addition to receipts, I jump online and look at our checking account and credit card.

Sometimes we misplace a receipt or never get one.

By checking online I find any I might otherwise miss.

Step #6: Review And Adjust

As the month progresses and you enter monthly expenses in your budget on a regular basis, you are going to see some interesting trends.

For now, you can cut back in some areas that you are overspending in if you feel as though the spending is out of control.

But just because you overspend this first month doesn’t mean you are doing something wrong.

Remember we took our best guess at how much we spend in each category.

Maybe you entered a number that is too low for you and you need to increase it.

This is why at first, I recommend you wait until month end to make adjustments.

See how everything works out and then make small changes to your budget from there.

If you find you spent less than you earned, you should move the difference into savings to help you get ahead.

If you find you spent more than you earned, then you need to do some work.

When this happens, it usually means you have been living beyond your means, which is another way of saying you are overspending.

When you do this, you will never get ahead financially.

By learning how to budget, we can correct this so that you can get out of debt, start saving and eventually reach your financial goals.

If you have to cut back, where do you make cuts and by how much?

We will tackle how much first.

We know the total amount of overspending already, we just have to break it into smaller pieces and spread it out.

For example, if you are over budget by $200, you can either pick a category and work to reduce that by $200 a month or you can pick 4 categories and reduce each by $50.

When it comes to where to cut expenses, there are some categories that are easier to work with than others.

- Read now: Learn over 100 ways to start saving money today

- Read now: Find out how to lower monthly bills by $1,000

An easy place to start is with variable expenses, more specifically, discretionary spending.

Are there some wants you’ve been spending money on that you can cut back a little bit?

Another place to look is food.

Stop eating out. When you go to the grocery store, buy what is on sale.

On the other hand, housing expenses might be difficult to reduce.

It isn’t easy to reduce your mortgage or rent.

You could shop around for insurance coverage, but other than that, your options are limited.

The key here is to look at everything and be honest with yourself as to what you are willing to cut down on your spending.

If you are having a hard time finding where to cut back, try using Trim.

- Read now: See how Trim saves users $625

This app will review your spending and give you suggestions on subscriptions to cancel.

It can also negotiate some of your bills for you as well, like your cable bill.

It’s free to try, so why not see how much money you can save?

Click on the link below to try it out.

Below is what my final budget looks like.

Note that I only did a handful of expenses in this example.

So I am keeping most of the budget categories the same.

But I do have money left over because our categories only account for 95% of our income.

I put it all this extra money into a savings account to beef up my emergency fund.

Step #7: Track And Adjust Some More

Now that you are in the second month of your budget, you should find things getting easier.

You should have a system for recording your living expenses and your categories should be getting closer to where you spend as well.

And while you still won’t be 100% accurate on the amounts you plan to spend in each category, it should be closer to reality.

Now you can start making adjustments during the month if you see you are overspending in one area.

You can either cut back or adjust your budget by taking some money from another category and moving it into that category.

After a few months of budgeting, you should also begin to review your spending compared to the previous month.

And ideally, the last couple of months.

This will help you to see trends with your spending and make a more realistic budget going forward.

Step #8: Dealing With The Unexpected

Especially in the first couple of months, while you are fine-tuning your budget, you may find yourself needing an emergency budget meeting in the middle of the month because unexpected expenses come up that you didn’t plan for.

Or you don’t have the money in the budget to cover it because it is more expensive than you thought, such as a car repair.

The meeting could be just you and your budget if you are on your own.

But if you are in a relationship, it should be you and your spouse with the budget even if one of you creates the budget and the other just signs off at the start.

The goal of the meeting is to discuss the expense and to find the money necessary to cover the expense in the budget while keeping the net at zero.

This means the household agrees to make whatever cuts are necessary in other categories to make sure the category that needs the money has the money to cover the expense.

For example, let’s say you budgeted $200 for car repairs this month, but the estimates you got to repair your car are actually $350.

In your budget meeting, you will discuss raising the car repair category by $150 to cover the repair, and you will both sign off on any adjustments in other categories to find $150 for that category.

Let’s say you agree to not go out to eat for a month, and that frees up $75.

You zero out that category and add that money to the car repair category.

Then, you agree that you don’t need to buy clothes this month, and that frees up another $75.

You then move that money into car repair, and re-do your math to make sure that your income and expenses remain equal and your budget nets out at zero.

Then you and your budget partner pinky-swear to hold to this budget for the rest of the month.

Budgeting Help

Now, with all this said, learning how to budget for the first time will take you some effort to set things up and get to the point where things are working.

I understand that you might not want to take the time to start a new budget from scratch.

But budgeting is the foundation for helping you to reach your financial goals, so it has to be done.

But is there an easier option?

Maybe speed up some of the setup and get right into budgeting?

After all, if others are budgeting, can’t you just copy their template and make adjustments?

Yes you can!

In fact, that is how I started off.

I wanted to save some time, so I searched around and found some great excel budget templates.

I narrowed down the one that looked like the best fit for me and got started.

I still had to make adjustments so it fit my life, but it was great to not have to start from scratch.

Of course, I know not everyone fits into this category of budgeters.

Maybe you want something a little more customizable to your liking.

Maybe you also want to save time by not having to manually record every single transaction you make.

If this is you, then Tiller Money is a great option.

It works using Google Sheets and it links up to your bank account.

It downloads your transactions so all you have to do is add a category label to them.

You can set up the sheet with graphs and charts and make it 100% your own.

And while it does cost money to use, you can try it out for free for 1 month when you click the link below.

Final Thoughts

There is a walk through to learn how to start budgeting.

I know the process can be overwhelming at first, but once you get started, it gets easier.

And after a couple of months, it gets addicting.

You get excited to see how your finances are doing and finally take control of your money.

You just have to be patient and have an open mind.

At the end of the day, always remember that a budget isn’t a tool that restricts your spending or freedom.

It is a tool to help you get to where you want to be financially.

And if you set yours up correctly, you can live and enjoy today while still meeting your future goals.

- Read now: Learn the 15 steps to building wealth

- Read now: Find out how to survive on $1,000 a month

- Read now: Learn how to calculate your net worth and get ahead

I have over 15 years experience in the financial services industry and 20 years investing in the stock market. I have both my undergrad and graduate degrees in Finance, and am FINRA Series 65 licensed and have a Certificate in Financial Planning.

Visit my About Me page to learn more about me and why I am your trusted personal finance expert.

I would recommend more frequent checkups than once a month. I like to review with my wife our budget at least once a week. The more often you do it, the easier it is to make little course corrections. 🙂

Good point Brock! It is easy to “forget” about small expenses you made throughout the month when trying to reconcile at month end. Plus, some receipts might go missing too.

I suggest to make a list of expenses and a budget for everyday. Doing this will surely help us save (plus the commitment to the plan). The process of budgeting looks so systematic.

I like to systematize too Jayson. It helps me to get into a habit more easily.

I agree with reviewing more often than once a month. In fact that’s part of why I installed YNAB on all my devices, so I could update my spending and see the impact on my budget as it happens. [My (grown) son uses Mint for the same purpose.]

That’s a great idea Jean! It sure makes it easier to not miss anything and to be up to date at all times.

Great tips! It’s the planning ahead for upcoming expenses that is either our saving grace or the major thorn in our side, depending on how well we’ve done it 🙂 Some months are better than others in this regard!

It’s always a learning process and I think you’ll never have it down perfectly. The key is just working on getting it right most of the time and having an emergency fund just in case for the ones your miss.

By tracking down your income and expenses would be a good help if you want to start a budget. You can use a spreadsheet budget or even downloading a mobile application.

There are all sorts of options out there, it’s just a matter of choosing a couple and finding which one works best for you.

You are absolutely correct – budgeting isn’t successful on the first or second try. It takes multiple attempts to see which one would work best, depending on your current status – there are instances where I do get off course but I do try to make up for it as soon as I get some extra money. This article helps a lot as I do have several goals I’d like to meet by the end of the year that only budgeting can help me achieve it in a major way. 🙂